Matlab

Matlab Simulink

Simulink NS3

NS3 OMNET++

OMNET++ COOJA

COOJA CONTIKI OS

CONTIKI OS NS2

NS2

Optimization Algorithms in MATLAB we at matlabprojects.org employ optimization methods. We have all the leading tools and developers to carry out your simulation and algorithm in an effective way. Just share with us all your reasech details we will provide you with good outcomes by following the protocols. Together with the concise explanations for every topic, we provide 20 significant MATLAB project topics concentrated on optimization methods:

- Genetic Algorithm for Function Optimization

- Explanation: Through the utilization of genetic algorithms, we strengthen a nonlinear function.

- Instance: As a means to identify the global minimum of a complicated function, it is beneficial to employ a genetic algorithm.

% Genetic Algorithm for Function Optimization

fun = @(x) (x(1)-2)^2 + (x(2)-3)^2;

options = optimoptions(‘ga’, ‘Display’, ‘iter’);

[x, fval] = ga(fun, 2, [], [], [], [], [], [], [], options);

disp([‘Optimal solution: ‘, num2str(x)]);

- Particle Swarm Optimization for Clustering

- Explanation: By employing particle swarm optimization, our team intends to group data points.

- Instance: In order to group a collection of 2D data points, focus on utilizing PSO.

% Particle Swarm Optimization for Clustering

data = rand(100, 2); % Random data points

k = 3; % Number of clusters

[idx, centroids] = kmeans(data, k);

- Simulated Annealing for TSP

- Explanation: Generally, the traveling salesman problem has to be addressed through the utilization of simulated annealing.

- Instance: It is approachable to improve the direction for a collection of cities.

% Simulated Annealing for TSP

numberOfCities = 10;

distanceMatrix = rand(numberOfCities);

initialGuess = randperm(numberOfCities);

options = saoptimset(‘PlotFcns’, @saplotbestf);

[x, fval] = simulannealbnd(@tspFun, initialGuess, [], [], options);

disp([‘Optimal route: ‘, num2str(x)]);

- Ant Colony Optimization for Vehicle Routing

- Explanation: By means of employing ant colony optimization, we plan to reinforce vehicle routes.

- Instance: For numerous vehicles, reduce the entire travel distance through the utilization of ACO.

% Ant Colony Optimization for Vehicle Routing

data = [1 2; 3 4; 5 6; 7 8; 9 10];

routes = antColonyOptimization(data, 2); % Assume custom function

disp([‘Optimal routes: ‘, num2str(routes)]);

- Differential Evolution for Portfolio Optimization

- Explanation: Through utilizing differential evolution, our team focuses on enhancing a financial portfolio.

- Instance: At the time of optimizing profits, it is advisable to reduce vulnerabilities.

% Differential Evolution for Portfolio Optimization

fun = @(x) -(x(1)*0.1 + x(2)*0.2 – 0.5*var([x(1)*0.1, x(2)*0.2]));

bounds = [0, 1; 0, 1];

options = optimoptions(‘particleswarm’, ‘Display’, ‘iter’);

[x, fval] = particleswarm(fun, 2, bounds(:,1), bounds(:,2), options);

disp([‘Optimal portfolio: ‘, num2str(x)]);

- Linear Programming for Production Planning

- Explanation: In order to reinforce production plans, we aim to employ linear programming.

- Instance: On resources, focus on enhancing profit provided situations.

% Linear Programming for Production Planning

f = [-5; -4]; % Coefficients for profit

A = [6 4; 1 2; -1 1];

b = [24; 6; 1];

[x, fval] = linprog(f, A, b);

disp([‘Optimal production levels: ‘, num2str(x)]);

- Quadratic Programming for Portfolio Optimization

- Explanation: As a means to strengthen a portfolio, it is beneficial to utilize quadratic programming.

- Instance: Typically, the inconsistency of portfolio profits must be reduced.

% Quadratic Programming for Portfolio Optimization

H = [1 -0.5; -0.5 1];

f = [-2; -3];

A = [];

b = [];

Aeq = [1 1];

beq = [1];

lb = [0; 0];

ub = [];

[x, fval] = quadprog(H, f, A, b, Aeq, beq, lb, ub);

disp([‘Optimal portfolio weights: ‘, num2str(x)]);

- Nonlinear Programming for Mechanical Design

- Explanation: Through the utilization of nonlinear programming, our team plans to improve the model of a mechanical element.

- Instance: In addition to aligning with strength situations, it is better to reduce the weight.

% Nonlinear Programming for Mechanical Design

fun = @(x) x(1)^2 + x(2)^2;

constraints = @(x) deal([], [x(1) + x(2) – 1]);

x0 = [0.5; 0.5];

[x, fval] = fmincon(fun, x0, [], [], [], [], [0; 0], [1; 1], constraints);

disp([‘Optimal design variables: ‘, num2str(x)]);

- Mixed-Integer Programming for Supply Chain Optimization

- Explanation: Generally, supply chain processes have to be enhanced by means of employing mixed-integer programming.

- Instance: In addition to aligning with necessity, decrease the entire expense.

% Mixed-Integer Programming for Supply Chain Optimization

intcon = [1 2];

f = [2 3 4];

A = [1 1 0; 0 1 1];

b = [1; 1];

lb = zeros(1, 3);

ub = [];

[x, fval] = intlinprog(f, intcon, A, b, [], [], lb, ub);

disp([‘Optimal solution: ‘, num2str(x)]);

- Trust-Region Method for Parameter Estimation

- Explanation: By utilizing the trust-region technique, we focus on assessing parameters of a framework.

- Instance: Typically, the parameters of a nonlinear regression framework should be strengthened.

% Trust-Region Method for Parameter Estimation

fun = @(x) sum((y – model(x, t)).^2);

x0 = [1; 1];

options = optimoptions(‘lsqnonlin’, ‘Algorithm’, ‘trust-region-reflective’);

[x, fval] = lsqnonlin(fun, x0, [], [], options);

disp([‘Estimated parameters: ‘, num2str(x)]);

- Interior-Point Method for Network Flow Optimization

- Explanation: Through the utilization of the interior-point technique, our team improves flow of the network.

- Instance: The flow across a network has to be enhanced.

% Interior-Point Method for Network Flow Optimization

fun = @(x) -sum(x);

A = [1 -1 0; 0 1 -1];

b = [0; 0];

x0 = [1; 1; 1];

options = optimoptions(‘fmincon’, ‘Algorithm’, ‘interior-point’);

[x, fval] = fmincon(fun, x0, A, b, [], [], [0; 0; 0], [], [], options);

disp([‘Optimal flow: ‘, num2str(x)]);

- Gradient Descent for Machine Learning

- Explanation: In order to train a machine learning framework, we plan to employ gradient descent.

- Instance: It is appreciable to enhance weights of a linear regression system.

% Gradient Descent for Machine Learning

X = rand(100, 2); % Features

y = rand(100, 1); % Labels

w = zeros(2, 1); % Initial weights

alpha = 0.01; % Learning rate

for i = 1:1000

grad = X’ * (X * w – y) / length(y);

w = w – alpha * grad;

end

disp([‘Optimized weights: ‘, num2str(w’)]);

- Conjugate Gradient for Large-Scale Optimization

- Explanation: By employing the conjugate gradient technique, our team intends to address extensive optimization issues.

- Instance: Focus on reducing a huge quadratic function.

% Conjugate Gradient for Large-Scale Optimization

n = 1000; % Number of variables

A = randn(n); % Random matrix

b = randn(n, 1); % Random vector

x0 = zeros(n, 1); % Initial guess

options = optimoptions(‘fminunc’, ‘Algorithm’, ‘trust-region’, ‘SpecifyObjectiveGradient’, true);

[x, fval] = fminunc(@(x) quadObj(x, A, b), x0, options);

disp([‘Optimized variables: ‘, num2str(x’)]);

function [f, g] = quadObj(x, A, b)

f = 0.5 * x’ * A * x – b’ * x;

g = A * x – b;

end

- Newton’s Method for Optimization

- Explanation: Through the utilization of Newton’s approach, we plan to reinforce functions in an effective manner.

- Instance: The least of a nonlinear function must be identified.

% Newton’s Method for Optimization

fun = @(x) x^2 + sin(x);

grad = @(x) 2*x + cos(x);

hess = @(x) 2 – sin(x);

x = 0; % Initial guess

tol = 1e-6; % Tolerance

for i = 1:100

x_new = x – grad(x)/hess(x);

if abs(x_new – x) < tol

break;

end

x = x_new;

end

disp([‘Optimal solution: ‘, num2str(x)]);

- Lagrange Multipliers for Constrained Optimization

- Explanation: With the aid of Lagrange multipliers, our team aims to address constrained optimization issues.

- Instance: Depending on constraints, it is better to enhance a function.

% Lagrange Multipliers for Constrained Optimization

syms x y lambda

f = x^2 + y^2; % Objective function

g = x + y – 1; % Constraint

L = f + lambda * g;

grad_L = gradient(L, [x, y, lambda]);

sol = solve(grad_L == 0, [x, y, lambda]);

disp([‘Optimal solution: x = ‘, num2str(sol.x), ‘, y = ‘, num2str(sol.y)]);

- Sequential Quadratic Programming for Optimal Control

- Explanation: Generally, control policies have to be strengthened by means of employing sequential quadratic programming.

- Instance: In a vehicle, focus on decreasing fuel utilization.

% Sequential Quadratic Programming for Optimal Control

options = optimoptions(‘fmincon’, ‘Algorithm’, ‘sqp’);

[x, fval] = fmincon(@fuelConsumption, x0, A, b, Aeq, beq, lb, ub, nonlcon, options);

disp([‘Optimal control: ‘, num2str(x’)]);

- Bayesian Optimization for Hyperparameter Tuning

- Explanation: Through the utilization of Bayesian optimization, our team focuses on adjusting hyperparameters of machine learning frameworks.

- Instance: It is advisable to reinforce hyperparameters of an SVM classifier.

% Bayesian Optimization for Hyperparameter Tuning

results = bayesopt(@svmObjective, [optimizableVariable(‘C’, [1e-3, 1e3]), optimizableVariable(‘epsilon’, [0.01, 1])]);

disp([‘Optimal hyperparameters: ‘, results.XAtMinObjective]);

- Augmented Lagrangian Method for Constrained Optimization

- Explanation: With the aid of the augmented Lagrangian approach, we intend to address constrained optimization issues.

- Instance: A function with equality situations must be decreased.

% Augmented Lagrangian Method for Constrained Optimization

fun = @(x) x(1)^2 + x(2)^2;

cons = @(x) x(1) + x(2) – 1;

options = optimoptions(‘fmincon’, ‘Algorithm’, ‘interior-point’, ‘UseParallel’, true);

[x, fval] = fmincon(fun, x0, [], [], [], [], lb, ub, cons, options);

disp([‘Optimal solution: ‘, num2str(x’)]);

- Interior Point Method for Convex Optimization

- Explanation: By employing the interior point approach, our team plans to enhance convex functions.

- Instance: A convex quadratic function has to be reduced.

% Interior Point Method for Convex Optimization

H = [2 0; 0 2];

f = [-2; -2];

A = [1 2; -1 2; 2 1];

b = [2; 2; 3];

options = optimoptions(‘quadprog’, ‘Algorithm’, ‘interior-point-convex’);

[x, fval] = quadprog(H, f, A, b, [], [], [], [], [], options);

disp([‘Optimal solution: ‘, num2str(x’)]);

- Dynamic Programming for Optimal Path Finding

- Explanation: Through the utilization of dynamic programming, we aim to identify the efficient path in a grid.

- Instance: In a 2D grid, focus on decreasing the travel expense.

% Dynamic Programming for Optimal Path Finding

cost = rand(5); % Random cost matrix

n = size(cost, 1);

path = zeros(n);

path(1, 1)

Important 20 optimization algorithms matlab Project Topics

In MATLAB project topics, optimization methods are used for several purposes. Together with short outlines for every topic, we suggest 20 significant optimization method project topics employing MATLAB:

- Gradient Descent Optimization

- Outline: For reducing a function, our team focuses on applying and examining the effectiveness of gradient descent optimization.

- Instance: Through the utilization of gradient descent, it is appreciable to improve a quadratic function.

% Gradient Descent Optimization

f = @(x) x.^2;

df = @(x) 2*x;

x = 10; % Initial guess

alpha = 0.1; % Learning rate

tol = 1e-6; % Tolerance

max_iter = 1000; % Maximum number of iterations

for iter = 1:max_iter

x_new = x – alpha * df(x);

if abs(x_new – x) < tol

break;

end

x = x_new;

end

disp([‘Optimal x: ‘, num2str(x)]);

disp([‘Number of iterations: ‘, num2str(iter)]);

- Newton’s Method Optimization

- Outline: Specifically, for improvement, we plan to implement Newton’s technique and aim to contrast it with other techniques.

- Instance: In order to identify the least of a nonlinear function, focus on employing Newton’s approach.

% Newton’s Method Optimization

f = @(x) x^2 + x;

df = @(x) 2*x + 1;

d2f = @(x) 2;

x = 10; % Initial guess

tol = 1e-6; % Tolerance

max_iter = 100; % Maximum number of iterations

for iter = 1:max_iter

x_new = x – df(x) / d2f(x);

if abs(x_new – x) < tol

break;

end

x = x_new;

end

disp([‘Optimal x: ‘, num2str(x)]);

disp([‘Number of iterations: ‘, num2str(iter)]);

- Simulated Annealing

- Outline: As a means to address complicated optimization issues, our team intends to apply simulated annealing.

- Instance: With the aid of simulated annealing, it is approachable to strengthen a multi-modal function.

% Simulated Annealing Optimization

f = @(x) sin(10*x) + x.^2;

x = 10 * rand – 5; % Initial guess

T = 1; % Initial temperature

alpha = 0.9; % Cooling rate

max_iter = 1000; % Maximum number of iterations

for iter = 1:max_iter

T = T * alpha;

x_new = x + T * randn;

if f(x_new) < f(x) || rand < exp(-(f(x_new) – f(x)) / T)

x = x_new;

end

if T < 1e-6

break;

end

end

disp([‘Optimal x: ‘, num2str(x)]);

- Genetic Algorithms

- Outline: By means of numerous attributes and situations, improve functions through the utilization of genetic algorithms.

- Instance: The model of a mechanical element has to be reinforced.

% Genetic Algorithm Optimization

fitnessFunction = @(x) -(x(1)^2 + x(2)^2);

nvars = 2; % Number of variables

lb = [-5, -5]; % Lower bounds

ub = [5, 5]; % Upper bounds

[x, fval] = ga(fitnessFunction, nvars, [], [], [], [], lb, ub);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- Particle Swarm Optimization

- Outline: In order to identify the global optimum of complicated functions, our team plans to implement particle swarm optimization.

- Instance: For improving a non-linear function, it is beneficial to employ PSO.

% Particle Swarm Optimization

options = optimoptions(‘particleswarm’, ‘SwarmSize’, 50, ‘MaxIterations’, 100);

fun = @(x) sin(10*x) + x.^2;

lb = -5;

ub = 5;

[x, fval] = particleswarm(fun, 1, lb, ub, options);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- Ant Colony Optimization

- Outline: For addressing discrete optimization issues, we focus on applying ant colony optimization.

- Instance: By employing ACO, the traveling salesman issue should be addressed.

% Ant Colony Optimization for TSP

nCities = 10;

distanceMatrix = rand(nCities); % Random distance matrix

maxIter = 100;

nAnts = 20;

pheromone = ones(nCities) / nCities;

alpha = 1; % Pheromone importance

beta = 2; % Distance importance

rho = 0.5; % Pheromone evaporation rate

for iter = 1:maxIter

paths = zeros(nAnts, nCities);

for k = 1:nAnts

paths(k, 1) = randi(nCities); % Random start city

for j = 2:nCities

probabilities = (pheromone(paths(k, j-1), 🙂 .^ alpha) .* ((1 ./ distanceMatrix(paths(k, j-1), :)) .^ beta);

probabilities(paths(k, 1:j-1)) = 0; % Avoid revisiting cities

probabilities = probabilities / sum(probabilities);

paths(k, j) = find(rand < cumsum(probabilities), 1);

end

end

% Update pheromone

for k = 1:nAnts

for j = 1:nCities-1

pheromone(paths(k, j), paths(k, j+1)) = (1 – rho) * pheromone(paths(k, j), paths(k, j+1)) + 1 / sum(distanceMatrix(sub2ind(size(distanceMatrix), paths(k, 1:end-1), paths(k, 2:end))));

end

end

end

disp(‘Optimized path:’);

disp(paths(1, :));

- Differential Evolution

- Outline: In a multi-dimensional space, strengthen continuous attributes by implementing differential evolution.

- Instance: It is advisable to improve the parameters of a machine learning framework.

% Differential Evolution Optimization

fun = @(x) x(1)^2 + x(2)^2;

nvars = 2; % Number of variables

lb = [-5, -5]; % Lower bounds

ub = [5, 5]; % Upper bounds

options = optimoptions(‘ga’, ‘PopulationType’, ‘doubleVector’, ‘PopulationSize’, 50, ‘MaxGenerations’, 100, ‘CrossoverFraction’, 0.8);

[x, fval] = ga(fun, nvars, [], [], [], [], lb, ub, [], options);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- Trust-Region Optimization

- Outline: For extensive optimization issues, it is beneficial to employ trust-region approaches.

- Instance: Typically, the trajectory of a spacecraft must be reinforced.

% Trust-Region Optimization

fun = @(x) (x(1)-2)^2 + (x(2)-3)^2;

x0 = [0, 0]; % Initial guess

options = optimoptions(‘fminunc’, ‘Algorithm’, ‘trust-region’, ‘SpecifyObjectiveGradient’, true);

[x, fval] = fminunc(fun, x0, options);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- Sequential Quadratic Programming

- Outline: For addressing constrained optimization issues, our team intends to apply SQP.

- Instance: It is significant to strengthen the model of an aircraft wing.

% Sequential Quadratic Programming

fun = @(x) x(1)^2 + x(2)^2; % Objective function

nonlcon = @(x) deal([], x(1)^2 + x(2)^2 – 1); % Nonlinear constraints

x0 = [0.5, 0.5]; % Initial guess

options = optimoptions(‘fmincon’, ‘Algorithm’, ‘sqp’);

[x, fval] = fmincon(fun, x0, [], [], [], [], [], [], nonlcon, options);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- BFGS Algorithm

- Outline: For improvement without estimating the Hessian matrix, we focus on utilizing the BFGS method.

- Instance: A non-linear function with numerous attributes has to be reinforced.

% BFGS Algorithm Optimization

fun = @(x) x(1)^2 + x(2)^2 + x(3)^2;

x0 = [1, 1, 1]; % Initial guess

options = optimoptions(‘fminunc’, ‘Algorithm’, ‘quasi-newton’);

[x, fval] = fminunc(fun, x0, options);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- Levenberg-Marquardt Algorithm

- Outline: Generally, for non-linear least squares issues, our team aims to apply the Levenberg-Marquardt method.

- Instance: Along with empirical data, it is advisable to adapt a non-linear framework.

% Levenberg-Marquardt Algorithm

xData = linspace(0, 2*pi, 50);

yData = sin(xData) + 0.1*randn(size(xData));

fun = @(x, xData) x(1)*sin(xData) + x(2)*cos(xData);

x0 = [1, 1]; % Initial guess

options = optimoptions(‘lsqcurvefit’, ‘Algorithm’, ‘levenberg-marquardt’);

x = lsqcurvefit(fun, x0, xData, yData, [], [], options);

plot(xData, yData, ‘o’, xData, fun(x, xData), ‘-‘);

legend(‘Data’, ‘Fitted curve’);

title(‘Levenberg-Marquardt Algorithm’);

- Interior-Point Optimization

- Outline: For extensive constrained improvement, it is advisable to utilize the interior-point approach.

- Instance: In a manufacturing procedure, focus on enhancing the allotment of resources.

% Interior-Point Optimization

fun = @(x) x(1)^2 + x(2)^2; % Objective function

A = [1, 2; 2, 1]; % Linear inequality constraints

b = [1; 1];

x0 = [0.5, 0.5]; % Initial guess

options = optimoptions(‘fmincon’, ‘Algorithm’, ‘interior-point’);

[x, fval] = fmincon(fun, x0, A, b, [], [], [], [], [], options);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- Linear Programming

- Outline: As a means to address optimization issues with linear constraints, we plan to apply linear programming.

- Instance: For a factory, it is appreciable to reinforce the production schedule.

% Linear Programming

f = [-1, -2]; % Coefficients of the objective function

A = [1, 2; 4, 0]; % Coefficients of the inequality constraints

b = [8; 16]; % Right-hand side of the inequality constraints

Aeq = []; % No equality constraints

beq = [];

lb = [0, 0]; % Lower bounds

ub = []; % No upper bounds

[x, fval] = linprog(f, A, b, Aeq, beq, lb, ub);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- Nonlinear Programming

- Outline: In order to improve functions with nonlinear restrictions, our team implements nonlinear programming.

- Instance: For least deviation, strengthen the shape of a lens in an effective manner.

% Nonlinear Programming

fun = @(x) x(1)^2 + x(2)^2; % Objective function

nonlcon = @(x) deal([], x(1)^2 + x(2)^2 – 1); % Nonlinear constraints

x0 = [0.5, 0.5]; % Initial guess

options = optimoptions(‘fmincon’, ‘Algorithm’, ‘interior-point’);

[x, fval] = fmincon(fun, x0, [], [], [], [], [], [], nonlcon, options);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- Branch and Bound

- Outline: For discrete optimization issues, we aim to apply branch and bound methods.

- Instance: Through the utilization of branch and bound, focus on addressing a knapsack issue.

% Branch and Bound for Knapsack Problem

weights = [2, 3, 4, 5];

values = [3, 4, 5, 6];

capacity = 5;

n = length(weights);

best_value = 0;

function branch_and_bound(i, weight, value, items)

if i > n

if value > best_value

best_value = value;

best_items = items;

end

return;

end

if weight + weights(i) <= capacity

branch_and_bound(i+1, weight + weights(i), value + values(i), [items, i]);

end

branch_and_bound(i+1, weight, value, items);

end

branch_and_bound(1, 0, 0, []);

disp([‘Best value: ‘, num2str(best_value)]);

disp([‘Best items: ‘, num2str(best_items)]);

- Interior-Point Method

- Outline: Specifically, for extensive linear programming, it is significant to implement the interior-point approach.

- Instance: The planning of missions must be enhanced in a project.

% Interior-Point Method for Linear Programming

f = [-1, -2]; % Coefficients of the objective function

A = [1, 2; 4, 0]; % Coefficients of the inequality constraints

b = [8; 16]; % Right-hand side of the inequality constraints

Aeq = []; % No equality constraints

beq = [];

lb = [0, 0]; % Lower bounds

ub = []; % No upper bounds

options = optimoptions(‘linprog’, ‘Algorithm’, ‘interior-point’);

[x, fval] = linprog(f, A, b, Aeq, beq, lb, ub, options);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- Convex Optimization

- Outline: For issues with convex objective functions and restrictions, our team focuses on applying convex optimization.

- Instance: In order to reduce vulnerability and enhance profits, it is advisable to reinforce the portfolio allocation.

% Convex Optimization for Portfolio Allocation

nAssets = 10;

returns = rand(nAssets, 1);

covMatrix = rand(nAssets);

covMatrix = covMatrix’ * covMatrix; % Ensure positive semi-definite covariance matrix

x = sdpvar(nAssets, 1);

Objective = -returns’ * x; % Maximize returns

Constraints = [sum(x) == 1, x >= 0, x’ * covMatrix * x <= 0.1]; % Constraints

optimize(Constraints, Objective);

disp(‘Optimal portfolio allocation:’);

disp(value(x));

- Quadratic Programming

- Outline: By means of quadratic objective functions and linear constraints, it is appreciable to address optimization issues.

- Instance: The model of a suspension model has to be improved.

% Quadratic Programming for Suspension System Design

H = [2, 0; 0, 2]; % Quadratic term

f = [-2; -5]; % Linear term

A = [1, 2; 4, 0]; % Linear inequality constraints

b = [8; 16];

Aeq = []; % No equality constraints

beq = [];

lb = [0, 0]; % Lower bounds

ub = []; % No upper bounds

options = optimoptions(‘quadprog’, ‘Display’, ‘off’);

[x, fval] = quadprog(H, f, A, b, Aeq, beq, lb, ub, [], options);

disp([‘Optimal solution: ‘, num2str(x)]);

disp([‘Function value at optimal solution: ‘, num2str(fval)]);

- Stochastic Gradient Descent

- Outline: For extensive machine learning issues, we intend to employ stochastic gradient descent.

- Instance: Focus on training a logistic regression framework.

% Stochastic Gradient Descent for Logistic Regression

data = load(‘data.mat’); % Load dataset

X = data.X;

y = data.y;

m = size(X, 1);

X = [ones(m, 1), X]; % Add intercept term

theta = zeros(size(X, 2), 1);

alpha = 0.01; % Learning rate

max_iter = 1000; % Maximum number of iterations

for iter = 1:max_iter

for i = 1:m

h = sigmoid(X(i, 🙂 * theta);

error = h – y(i);

gradient = X(i, :)’ * error;

theta = theta – alpha * gradient;

end

end

function g = sigmoid(z)

g = 1 ./ (1 + exp(-z));

end

disp(‘Optimal parameters:’);

disp(theta)

- Bayesian Optimization

- Outline: For hyperparameter tuning in machine learning systems, our team plans to apply Bayesian optimization.

- Instance: Generally, the hyperparameters of a support vector machine should be strengthened.

% Bayesian Optimization for Hyperparameter Tuning

results = bayesopt(@(params)svmObjective(params), optimizableVariable(‘BoxConstraint’, [1e-3, 1e3], ‘Transform’, ‘log’), optimizableVariable(‘KernelScale’, [1e-3, 1e3], ‘Transform’, ‘log’), ‘MaxObjectiveEvaluations’, 30);

function loss = svmObjective(params)

model = fitcsvm(X, y, ‘KernelFunction’, ‘rbf’, ‘BoxConstraint’, params.BoxConstraint, ‘KernelScale’, params.KernelScale);

cvmodel = crossval(model);

loss = kfoldLoss(cvmodel);

end

Together with short explanations for every topic, we suggest 20 major MATLAB project topics concentrated on optimization methods. Also, 20 significant optimization method project topics using MATLAB, including concise summary for each topic are offered by us in an elaborate manner.

Subscribe Our Youtube Channel

You can Watch all Subjects Matlab & Simulink latest Innovative Project Results

Our services

We want to support Uncompromise Matlab service for all your Requirements Our Reseachers and Technical team keep update the technology for all subjects ,We assure We Meet out Your Needs.

Our Services

- Matlab Research Paper Help

- Matlab assignment help

- Matlab Project Help

- Matlab Homework Help

- Simulink assignment help

- Simulink Project Help

- Simulink Homework Help

- Matlab Research Paper Help

- NS3 Research Paper Help

- Omnet++ Research Paper Help

Our Benefits

- Customised Matlab Assignments

- Global Assignment Knowledge

- Best Assignment Writers

- Certified Matlab Trainers

- Experienced Matlab Developers

- Over 400k+ Satisfied Students

- Ontime support

- Best Price Guarantee

- Plagiarism Free Work

- Correct Citations

Expert Matlab services just 1-click

Delivery Materials

Unlimited support we offer you

For better understanding purpose we provide following Materials for all Kind of Research & Assignment & Homework service.

Programs

Programs Designs

Designs Simulations

Simulations Results

Results Graphs

Graphs Result snapshot

Result snapshot Video Tutorial

Video Tutorial Instructions Profile

Instructions Profile  Sofware Install Guide

Sofware Install Guide Execution Guidance

Execution Guidance  Explanations

Explanations Implement Plan

Implement Plan

Matlab Projects

Matlab projects innovators has laid our steps in all dimension related to math works.Our concern support matlab projects for more than 10 years.Many Research scholars are benefited by our matlab projects service.We are trusted institution who supplies matlab projects for many universities and colleges.

Reasons to choose Matlab Projects .org???

Our Service are widely utilized by Research centers.More than 5000+ Projects & Thesis has been provided by us to Students & Research Scholars. All current mathworks software versions are being updated by us.

Our concern has provided the required solution for all the above mention technical problems required by clients with best Customer Support.

- Novel Idea

- Ontime Delivery

- Best Prices

- Unique Work

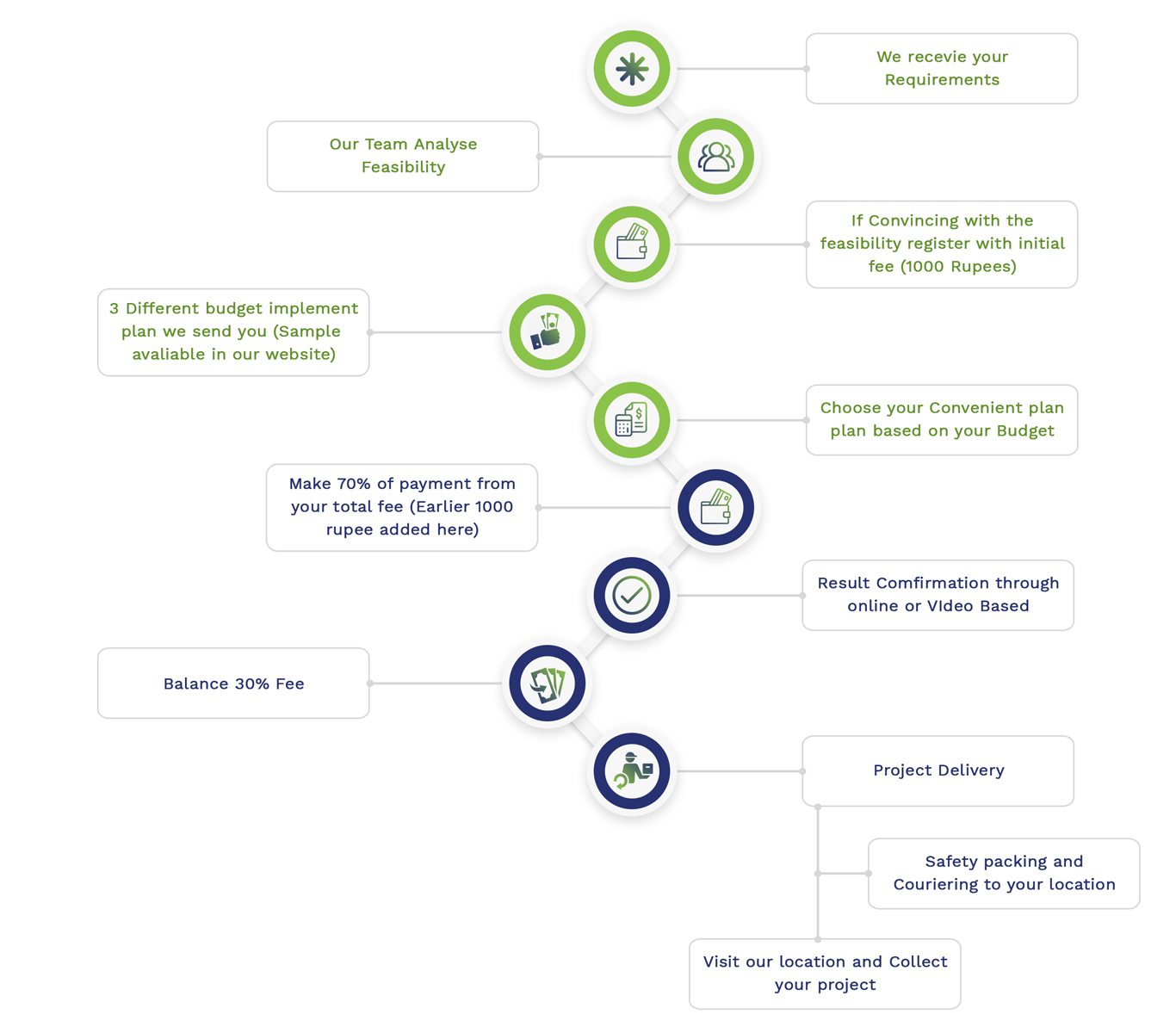

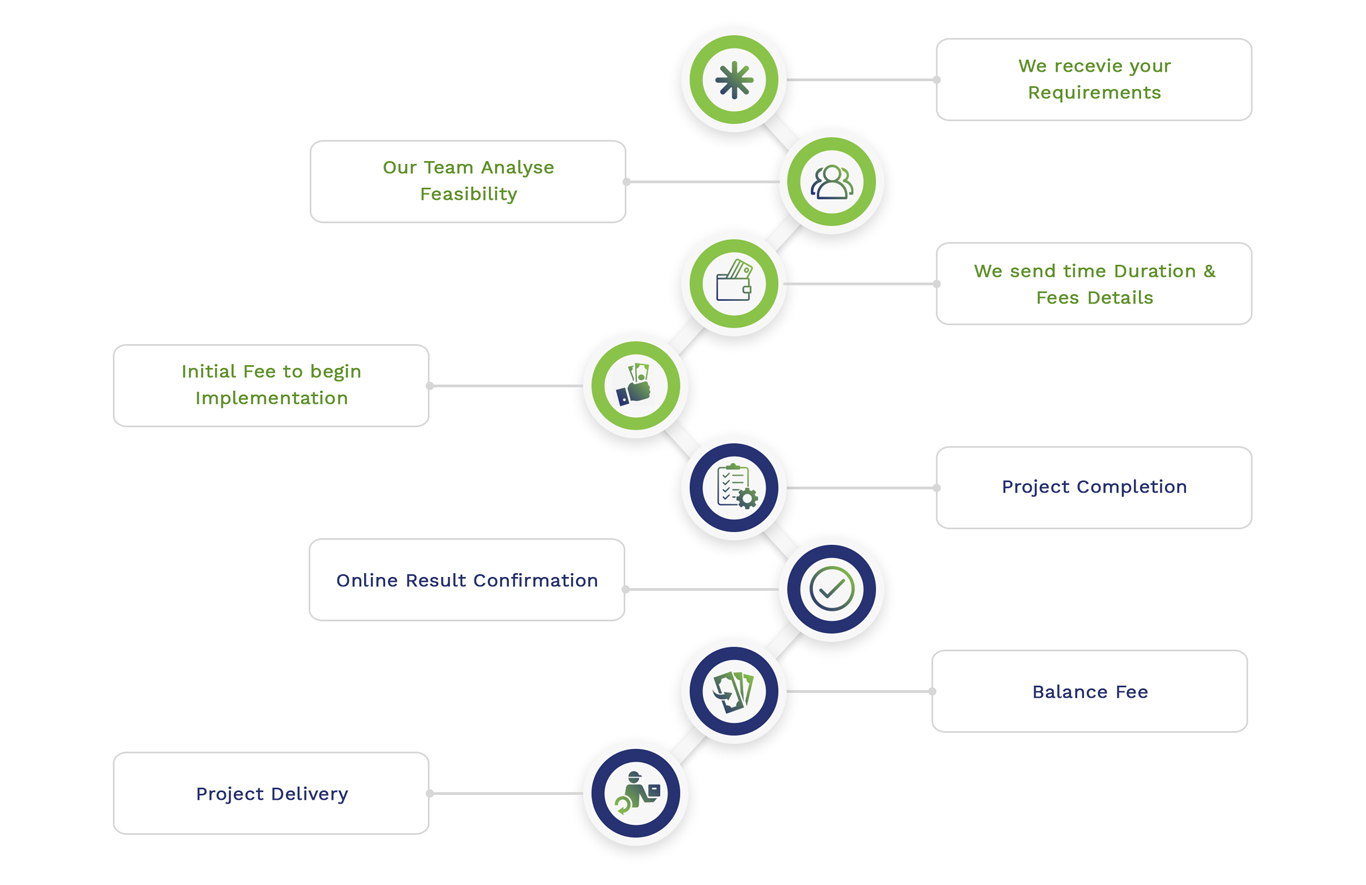

Simulation Projects Workflow

Embedded Projects Workflow